COMMON MISTEAKS

MISTAKES IN

USING STATISTICS: Spotting and Avoiding Them

Using confidence

intervals when prediction intervals are needed

As pointed out in the discussion of overfitting in regression, the model

assumptions for least squares regression assume that the conditional

mean function E(Y|X = x) has a

certain form; the regression estimation procedure then produces a

function

of the specified form

that estimates the true conditional mean function.

For example, if the model assumption is that

E(Y|X=x) = α

+βx,

then least squares regression will produce an equation of the form

y = a

+bx,

where a is an estimate of the true value α

and

b is an estimate of the true value β.

Thus for a particular

value of x,

ŷ = a

+bx

is the estimate of E(Y|X = x).

But now suppose we want to estimate

an actual value of Y when X =

x, rather than just the conditional mean E(Y|X = x). The

only estimate available for an actual value of Y is ŷ

= a

+bx, the same thing we used to estimate E(Y|X

= x). But since Y

is a random variable (whereas E(Y|X = x) is a single number, not a

random variable), we cannot

expect to estimate Y as precisely as we

can estimate the conditional mean E(Y|X=x);

i.e., even if ŷ is a good estimate of the

conditional mean E(Y|X = x), it might be a very

crude

estimate of an actual value of Y.

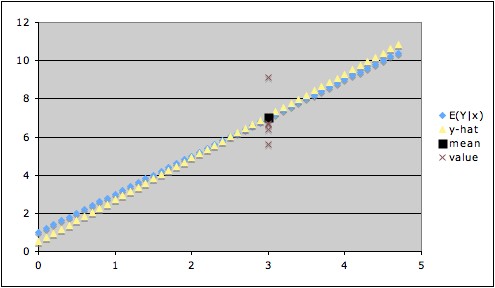

The graph below illustrates this. The

blue line is the actual line

of conditional means, the yellow

line is

the calculated regression line, the brown

x's show some values of Y when x = 3,

and the black square shows

the value of the conditional mean of Y when

x = 3. In this example, the estimate ŷ for x = 3

is

virtually indistinguishable from the conditional mean when x = 3,

so ŷ is a very good estimate of the

conditional mean. But if we are trying to estimate Y when x = 3, our

estimate ŷ (black square) might be way off --

for example, the

value of Y might turn out to be at the highest brown x or at the

lowest. This illustrates how the

uncertainty of ŷ

as an estimate of Y is much greater than the uncertainty of ŷ

as an estimate of the conditional mean of Y.

To estimate the uncertainty in our estimate of the

conditional mean E(Y|X = x), we can construct a confidence interval for the conditional mean. But, as

we have seen, the uncertainty in our estimate of Y when X = x is

greater than our uncertainty of E(Y|X = x). Thus, the confidence interval for the

conditional mean underestimates

the uncertainty in our use of ŷ as an estimate of a value of Y|(X = x).

Instead, we need what is called a prediction interval,

which takes into account the variability in the conditional

distribution Y|(X = x) as well as the uncertainty in our estimate of

the conditional mean E(Y|(X = x).

Example:

With the data used to

create the above plot, the 95% confidence interval for the conditional

mean when x = 3 is (6.634, 7.568) (giving a margin of error of about

0.5) , and the 95% prediction interval for Y when x = 3 is (5.139,

9.062) (giving a margin of error of about 2) .

(Note that the prediction interval includes all of the y-values

associated with x = 3 in the data used, except for the highest one,

which it misses by a hair.)

Comments:

1. For large enough sample size, the least squares estimate of the

conditional mean is fairly robust to departures from the model

assumption of normality of errors. This depends on the Central Limit

theorem and the fact that the formula for ŷ

can be expressed as a linear combination of the y-values for the data.

However, since the t-statistic used in calculating the prediction

interval also involves the conditional distribution directly, prediction is less robust to departures

from normality.

2. The distinction between variability

and uncertainty is useful in understanding the distinction between

confidence intervals for the conditional mean and prediction intervals:

The confidence interval for the conditional mean measures our degree of

uncertainty in our estimate of

the conditional mean; but the prediction interval must also take into

account the variability in

the conditional distribution1.

Notes:

1. In fact, for least squares simple linear regression,

- The width of the confidence

interval depends on the variance of ŷ =

ax + b

as an estimator of E(Y|X = x),

- whereas the width of the prediction

interval depends on the variance of ŷ

as an estimator of Y|(X = x).

- The variance of ŷ as an

estimator of Y|(X = x) is the

sum of the conditional variance (usually denoted σ2)

and the variance of ŷ as an estimator of

E(Y|X = x).

- The first term (σ2)

is a measure of the variability in the

conditional distribution;

- the second term (the variance of ŷ

as an estimator of

E(Y|X = x)) is a measure of the uncertainty in

the estimate of the conditional mean.

- The conditional variance σ2

typically is the larger of these two terms.